Interchange fee

is a term used in the credit card processing

industry and it describes a percentage fee

that a merchant account bank (the bank that

provides a merchant account for a business

- also called “acquiring bank”)

pays a cardholder’s bank (the “issuing

bank”). This fee is paid each and

every time a merchant takes an online payment

for its products and services from an Internet

shopper.

When merchants accept cards

like Visa or MasterCard for purchases, the

issuing bank (the bank that issued the credit

card to the Internet shopping using that

card) deducts the interchange fee from the

amount it pays back to the acquiring bank

that handles a credit or debit card transaction

for a merchant. For more description on

this, refer to Accepting

Credit Cards online.

The acquiring bank then

pays the merchant the amount of the transaction

minus both the interchange fee and any additional

fees that it charges for its own services

which is usually much smaller fee for the

acquiring bank.

While credit card purchasing

in the United States currently exceeds $1.5

trillion annually, the number of banks issuing

credit cards have been reduced dramatically

due to takeovers, acquisitions and mergers.

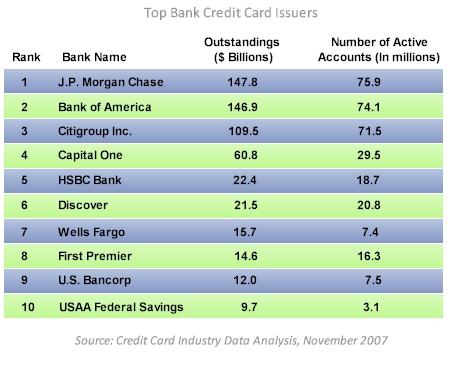

The top five credit

card issuing banks now control more than

90% of all credit card accounts and earn

more than $40 billion annually from interchange

fees, an increase of 90% since 2001.

The Interchange fees are

set by the credit card associations such

as VISA or MasterCard, and are by far the

largest component of the various fees that

banks deduct from merchants' credit card

sales, representing about 80% of these fees.

These fees are also

the subject of several ongoing lawsuits

in the United States.

Interchange fees are based

on the credit card brand, the type of credit

or debit card, the type and size of the

accepting merchant, and the type of transaction

(e.g. Internet, Retail, MOTO, Hotel, Airline,

etc.).

To make the

rates schedules even more complex, Interchange

fees are typically a flat fee plus

a percentage of the total purchase price

(including taxes). In the United States,

the fee averages approximately 2% of transaction

value. In other countries the Interchange

fees are substantially lower.

0.44% - Australia

0.44% - Australia

0.80% - EU Cross Border

0.80% - Denmark

0.80% - UK

0.92% - Italy

0.90% - Sweden

0.95% - New Zealand

1.05% - Honk Kong

1.00% - Brazil

1.15% - Singapore

1.17% - Malaysia

1.38% - Belgium

1.60% - Greece

2.00% - United States

0.44% - Australia

0.44% - Australia

0.44% - Australia

Interchange fees are indeed

a controversial issue and have been the

subject of regulatory and antitrust investigations

by the U.S. Federal government. Only very

large merchants have the leverage to negotiate

these fees and in some cases the Interchange-driven

prices exceed the small retailers' profit

margin.

Merchant Account

Discount Rate

Visa and Master card merchant

account discount rates should be TOTAL of

2.1%. This is broken into Interchange fee

(1.9%) for the issuing bank and the Plus

fee (0.2) for the acquiring bank. What seems

to unfair to me is the the issuing bank

really doesn't do anything other than issue

a credit card. It is the Acquiring bank

that takes on all the risk associated to

the transaction on behalf of the merchant

and it only ends up with 0.2% of the sale.

There are currently investigations

being performed by various agencies to establish

validity of merchants' accusations that

the Interchange fees represent “price

fixing” by VISA and MasterCard associations

like a “cartel” .

Consumer that pay with cash

are also uneasy about this since the

merchant costs increase due to the Interchange

fees and hence customers who pay with cash

or checks end up subsidizing purchases by

card users.

Also a very important point

is the the Interchange

fees are way too high in the United States

compared to most Western and industrialized

nations elsewhere in the world. There is

no justification for this difference especially

since the U.S. is the pioneer of the VISA

and MasterCard Associations and card technology).

It is also quite unfair

and against fairness in market economy when

few merchants like Wal-Mart can negotiate

an exception to the Interchange fees but

smaller businesses cannot.

Finally, the rising fees

association to the Interchange pricing structure

is by no means reasonable as the every cost

of payment processing, networking, infrastructure

developing, borrowing, fraud prevention,

chargebacks, and banking costs have declined

consistently over the last 10 years.

|